Casino operators are fundamentally rethinking portfolio construction as market data reveals that success in 2026 depends less on title volume and more on strategic content allocation. The emerging consensus centres on a deliberate 40/40/20 distribution model that prioritises revenue stability over pure slot-driven GGR maximisation.

The shift addresses a critical vulnerability in most operator lobbies: concentration risk. While slots consistently generate 70% to over 80% of online casino GGR in European regulated markets according to ~70–80% of online casino GGR, over-reliance on a single category creates revenue volatility and limits demographic conversion potential.

Portfolio Architecture: Beyond Slot Dominance

The 40/40/20 framework assigns distinct commercial roles across three tiers:

- 40% Acquisition: High-velocity RNG-based games, primarily slots, driving top-of-funnel traffic and first-deposit conversion

- 40% Retention: High-turnover community-driven assets, focusing on live table games for revenue stability and VIP concentration

- 20% Engagement & Diversification: Mobile-first formats including crash, arcade, and instant-win games targeting non-traditional demographics

This allocation reflects operational realities rather than rigid mandates. Mobile-heavy markets in Southeast Asia and Sub-Saharan Africa may warrant higher engagement tier weighting, while VIP-focused brands in mature European markets could tilt toward live casino within the retention category.

The framework addresses demographic conversion challenges. Traditional slot and live casino content frequently fails to convert the 18 – 24 demographic, which records the strongest growth rate across all age segments in online gambling at approximately 12% CAGR. Meanwhile, users aged 25-34 already represent 34.1% of the global online gambling customer base, creating pressure for format diversification.

| Tier | Weight | Category | Purpose |

|---|---|---|---|

| Acquisition | 40% | High-velocity, RNG-based games (e.g., slots) | Drive top-of-funnel traffic and first-time deposits |

| Retention | 40% | High-turnover, community-driven assets (e.g., live table games) | Revenue stability and VIP concentration |

| Engagement & Diversification | 20% | Participatory, mobile-first formats (e.g., crash, fishing games) | Convert non-traditional demographics |

The 40/40/20 Framework

This strategic allocation model assigns 40% to acquisition-focused slots, 40% to retention-driven live casino, and 20% to mobile-first engagement formats. The framework addresses concentration risk while targeting non-traditional demographics that traditional content fails to convert.

This appears to be an incomplete word at the end of the article and should be removed or completedastructure Considerations: Direct vs. Aggregated Content

Implementing balanced portfolios at scale – 5,000 to 10,000+ titles – creates operational complexity. Direct integration offers stronger commercial terms but typically requires 12 – 18 months for onboarding 50+ providers, placing significant strain on engineering teams through individual API integrations, compliance vetting, and ongoing maintenance.

Game aggregation addresses this infrastructure challenge through single API connections that centralise content access, reporting, and compliance oversight. Solutions like the SOFTSWISS Game Aggregator provide immediate access to certified, globally accessible libraries with GEO-specific selection and pre-certified content for regulated jurisdictions.

| Approach | Speed to Market | Technical Maintenance | Reporting | Compliance |

|---|---|---|---|---|

| Direct Integration | 12 – 18 months for 50+ studios | Operator manages all updates | Fragmented dashboards | Individual studio vetting |

| Aggregation | Days to weeks for 10,000+ titles | Handled by aggregator | Unified back-office | Pre-certified content |

Pros

- Days to weeks for 10,000+ titles vs 12-18 months

- Unified back-office reporting across all providers

- Pre-certified content for regulated jurisdictions

- Technical maintenance handled by aggregator

Cons

- Higher volume-based fees vs direct integration

- Less control over individual provider relationships

- Dependency on aggregator's technical infrastructure

- Potentially weaker commercial terms than direct deals

Slots: Acquisition Engine with Format Variations

Online slots remain the primary acquisition tool, with European regulated markets generating double-digit year-on-year growth across the continent in 2024, with overall online GGR rising 11.7% to €47.9 billion, according to the EGBA European Gambling Market Key Figures 2025 Edition.

Different slot formats serve distinct commercial purposes:

Classic Slots

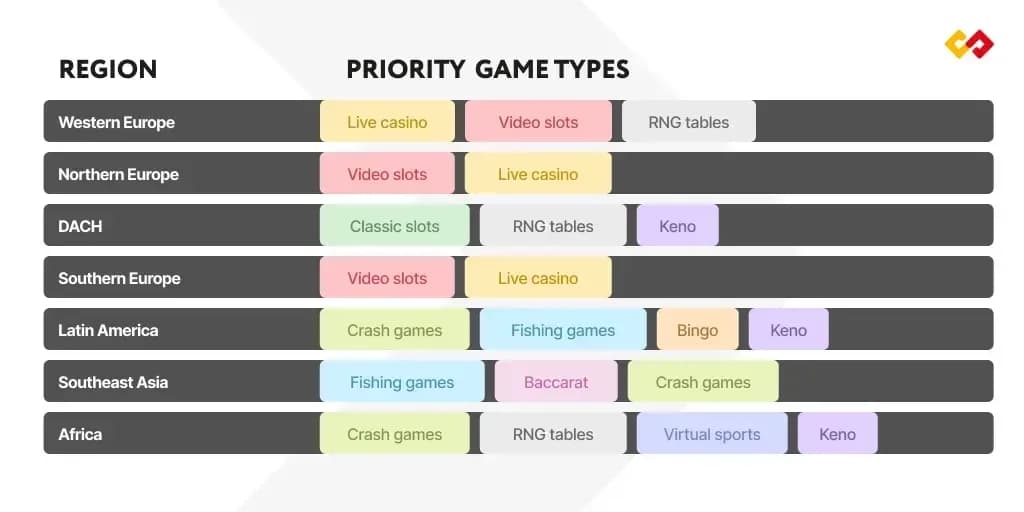

Three-reel, low-complexity titles replicating physical fruit machines target purist segments in DACH and Eastern Europe where land-based nostalgia drives acquisition. Studios like Amatic and Amusnet (EGT Interactive) maintain catalogues focused on this format.

Video Slots

Modern five-reel titles with narrative themes and layered bonus features serve as the primary acquisition tool for contemporary demographics in the Nordics, Canada, and Latin America. Pragmatic Play, BGaming, Push Gaming, and Nolimit City operate at volume here, releasing new titles monthly.

Megaways™ Slots

Originated by Big Time Gaming and now widely licensed, these titles create up to 117,649 ways to win per spin through variable symbol counts on each reel. The extreme variance targets sophisticated high-value players actively seeking risk exposure.

Progressive Slots & Jackpots

Networked titles pool portions of every bet into shared prize structures, often reaching millions. Large jackpot figures generate organic acquisition through press coverage, social sharing, and player word-of-mouth at costs that paid media cannot replicate. The SOFTSWISS Jackpot Aggregator enables networked progressive prizes without independent pooled prize management.

Jackpot Marketing Strategy

Large jackpot figures generate organic acquisition through press coverage and social sharing at costs that paid media cannot replicate. This makes progressive slots valuable beyond their direct GGR contribution.

RNG Table Games: Digital Foundation for Global Markets

Digital roulette and blackjack together typically account for 10 – 15% of online casino GGR in European regulated markets, though this varies significantly by demographic and geography. With no wait times, lower bet thresholds, and continuous availability, they drive session frequency and extend player lifetime value.

Mobile dominance – accounting for 58% of online gambling revenue across Europe – makes RNG table games essential infrastructure. Where HD live dealer streaming proves unviable across much of Africa and Latin America, they deliver complete casino experiences without bandwidth dependency.

Blackjack

Player decisions create skill layers that drive repeat sessions. With optimal basic strategy, the theoretical house edge can reach as low as 0.5%, making it among the most player-friendly RNG formats. NetEnt, Relax Gaming, and Groove Studios maintain strong blackjack portfolios.

Roulette

Digital wheel simulations provide foundational table lobby content. Operators can source classics or specific variants from Evolution (First Person Lightning Roulette), Pragmatic Play (Mega Roulette), and Amusnet (Virtual Vegas Roulette).

Baccarat

Fixed drawing rules, instant results, and strong cultural familiarity in Asian markets make this a priority title for operators targeting that segment. Evolution and Pragmatic Play offer comprehensive baccarat variations.

Craps

Full digital betting layouts with RNG-determined dice results across complete wager type ranges. Vivo Gaming and Live Solutions provide craps offerings for operators requiring this format.

70-80%

Slots' share of online casino GGR in European markets

40/40/20

Strategic portfolio distribution model

12%

CAGR growth rate for 18-24 demographic

34.1%

25-34 age group's share of global online gambling base

€47.9 billion

European online GGR in 2024

11.7%

Year-on-year growth in European regulated markets

58%

Mobile's share of European online gambling revenue

0.5%

Blackjack house edge with optimal basic strategy

Live Casino: VIP Revenue Concentration

Live dealer games combine physical game credibility with online convenience through streaming human croupiers to player screens. The segment projects 11.83% CAGR growth through 2031, outpacing the broader casino market, while live/in-play wagering already accounts for 53.4% of all betting activity in 2025.

Live casino generated an estimated €3.4 billion in 2025 from a total European online casino market of €25.6 billion. The core remains live baccarat and blackjack, but the most significant commercial evolution occurs in live game shows competing directly for attention against streaming platforms.

Titles like Evolution's Monopoly Live and Funky Time blend high-fidelity AR with real-time human interaction, transforming sessions into primary entertainment choices rather than transactional gambling experiences. Studios to consider include Ezugi and CreedRoomz for diverse live offerings.

Warning

The UK's Remote Gaming Duty increase to 40% in April 2026 is already affecting content economics for studios. Operators must factor compliance costs into provider selection and content economics planning.

Hybrid Games: Converting Mobile-First Demographics

Hybrid formats have become core portfolio requirements for reaching mobile-first and younger players who traditional content fails to convert effectively.

Crash Games

Players watch multipliers climb from 1× until RNG-determined crash points, deciding when to cash out. Spribe's Aviator processed €160 billion in total play volume in 2025, with approximately 17.4 billion bets per month at peak activity in 2024. Operators adding Aviator report GGR uplifts of at least 10%.

Crash games represent approximately 1.1% of European digital casino GGR – around €2.56 billion – but their real growth story unfolds outside Europe. Markets in Africa, Latin America, and Southeast Asia helped push Aviator's monthly players from 42 million to over 77 million within a single year.

Spribe's Aviator and SmartSoft's JetX serve as category benchmarks, while BGaming and Gamzix offer proven alternatives with strong emerging market performance.

Crash Game Performance Data

Spribe's Aviator processed €160 billion in total play volume in 2025, with approximately 17.4 billion bets per month at peak activity. Operators adding Aviator report GGR uplifts of at least 10%, demonstrating the category's commercial impact.

Fishing Games

Players aim and shoot at moving targets to earn multipliers, combining resource management with continuous decision-making. The mechanics sit closer to video gaming than traditional gambling – a deliberate design choice driving strong performance in Latin America and Asia. KA Gaming, Spadegaming, and TaDa Gaming offer high-engagement fishing titles.

Casual & Instant Win Games

Scratch cards, mines, plinko, dice, and hi-lo formats comprise the short-session segment projected to reach 6.98 billion euro by 2032 at a 13.6% CAGR. Minimal learning curves make them effective for reactivation campaigns, sportsbook cross-sell, and session frequency uplift. Hacksaw Gaming, Evoplay, and SmartSoft maintain strong portfolios in this space.

Portfolio Diversification Categories

Virtual Sports

RNG-driven simulations of football, horse racing, and cycling running on continuous schedules provide familiar betting structures without calendar dependency for sports-betting audiences crossing into online casino. They load efficiently in low-bandwidth markets. 1X2gaming and Golden Race offer comprehensive virtual sports portfolios covering football leagues, racing events, and continuously scheduled simulations.

Bingo

Players mark called numbers on cards; first pattern completion wins. Frequently underestimated outside core markets, bingo generates habitual return behaviour through shared draws and community mechanics that slots and table games cannot replicate. Essential for UK, Nordic, or Latin American operations. Relax Gaming and Amusnet offer strong regulated-market coverage.

Keno

Players select numbers from ranges and win based on draw matches. Fast rounds, zero learning curves, and strong cultural familiarity in lottery-oriented markets make it a reliable mobile-first casual format. SmartSoft Gaming provides keno options for operators requiring this format.

Provider Selection Framework

Studio selection represents procurement decisions with long-term operational consequences. Evaluation criteria include:

Regulatory Certification: Verify licences per jurisdiction. The UK's Remote Gaming Duty increase to 40% in April 2026 already affects content economics for studios operating there.

Game Mathematics: Confirm RTPs per title – most regulated markets mandate 92 – 96% minimums. Also verify variance profiles, hit frequencies, and math model documentation affecting player experience and responsible gambling compliance in markets like the UK and Netherlands.

RNG Certification: Confirm independent certification from recognised testing laboratories – eCOGRA, iTech Labs, or GLI. This represents a prerequisite for regulated market deployment.

Portfolio Coverage and Release Cadence: Assess coverage across relevant categories and release schedules as proxies for content pipeline health, balanced with average title performance and intellectual property strength.

Technical Reliability: Review uptime SLAs and incident response times. VIP tolerance for downtime remains low, particularly in live casino environments.

Promotional Tooling: Confirm support for free rounds, prize drops, and tournaments, whether triggered from platforms or requiring studio-side configuration.

Analytics and Reporting: Verify availability of game-level performance data – session length, hit frequency in practice, volatility distribution – supporting placement and promotional decisions.

For operators sourcing content via aggregation, most criteria are addressed at infrastructure levels, streamlining the evaluation process.

How to Evaluate Game Providers

Verify Regulatory Certification

Confirm licences per jurisdiction and check compliance with local RTP requirements (typically 92-96% minimums)

Assess Technical Infrastructure

Review uptime SLAs, incident response times, and RNG certification from recognized testing laboratories like eCOGRA or iTech Labs

Evaluate Portfolio Coverage

Assess coverage across relevant categories, release schedules, and promotional tooling support for free rounds and tournaments

Analyze Performance Metrics

Review game-level analytics availability, hit frequency data, and variance profiles supporting placement decisions

Performance Measurement Standards

Well-structured portfolios require category-level measurement through specific KPIs:

GGR per Active Title: Set category-level thresholds and remove underperforming titles on rolling bases. Flag any title generating materially less than fair-share category GGR after 60 – 90 days of active placement. Measure against theoretical GGR (turnover × house edge) rather than raw GGR to account for RTP differences.

Category-Level LTV: Track by game category beyond overall metrics. Internal operator data suggests crash game players may generate significantly higher LTV than slot players – with multipliers of 3× or more reported anecdotally – though this varies by operator type, demographic, and market.

Lobby-to-Play Conversion Rate: Low conversion typically indicates poor architecture or content imbalance rather than acquisition problems.

Cross-Category Play Rate: Higher cross-category engagement correlates with longer retention and higher LTV. Operators actively cross-promoting between live casino, slots, and crash formats report higher session frequency and stronger retention than single-category-dominant operations.

Reactivation Response by Format: Track which formats drive highest return rates in reactivation campaigns. Instant-win and crash games frequently outperform slots in this context.

Cross-Category Engagement Impact

Higher cross-category engagement correlates with longer retention and higher LTV. Operators actively cross-promoting between live casino, slots, and crash formats report higher session frequency and stronger retention than single-category-dominant operations.

Responsible Gambling Integration

Responsible gambling represents a core operational requirement rather than layered addition. Operators must build player protection directly into products:

- Transparent Game Information: Clear RTP displays on all titles

- Spend Controls: Deposit limits and session timers accessible by default

- Behavioural Safeguards: Bonus mechanics audited for loss-chasing incentives and support teams trained for early risk signal recognition

In practice, video slots published in competitive regulated markets typically display RTPs in the 94 – 97% range, reflecting player expectations. Progressive jackpot titles commonly carry lower base RTPs of 88 – 94% as portions of every wager fund shared prize pools.

Strategic Portfolio Implications

The transition from volume-based to allocation-based portfolio thinking reflects broader industry maturation. Operators building around the 40/40/20 model position themselves for more stable revenue generation while capturing demographic segments that traditional slot-heavy lobbies miss.

The model's effectiveness depends on execution quality rather than strict adherence. Market-specific adjustments remain essential – mobile-heavy regions may warrant higher engagement tier allocation, while VIP-focused operations might emphasise live casino within retention categories.

Infrastructure choices significantly impact implementation feasibility. Aggregation solutions enable rapid deployment of balanced portfolios without the extended integration timelines that direct provider relationships typically require, particularly when targeting comprehensive coverage across all three allocation tiers.

The regulatory environment continues shaping portfolio decisions. The UK's upcoming Remote Gaming Duty increase exemplifies how compliance costs affect content economics, while varying RTP requirements across jurisdictions influence provider selection and title placement strategies.

The transition from volume-based to allocation-based portfolio thinking reflects broader industry maturation, positioning operators for more stable revenue generation while capturing demographic segments that traditional slot-heavy lobbies miss.

The model assigns 40% to acquisition-focused games (primarily slots), 40% to retention-driven content (mainly live casino), and 20% to engagement formats (crash games, instant win). This framework addresses concentration risk while targeting diverse demographics that traditional content fails to convert.

Aggregation enables access to 10,000+ titles within days to weeks versus 12-18 months for direct integration of 50+ providers. It provides unified reporting, pre-certified content, and eliminates technical maintenance burden while reducing engineering strain.

Crash games represent approximately 1.1% of European digital casino GGR (around €2.56 billion). However, operators adding Aviator report GGR uplifts of at least 10%, with the format showing particularly strong performance in emerging markets outside Europe.

Essential KPIs include GGR per active title with category-level thresholds, cross-category play rates, and reactivation response by format. Higher cross-category engagement correlates with longer retention and higher lifetime value across all player segments.

The UK's Remote Gaming Duty increase to 40% in April 2026 exemplifies how compliance costs affect content economics. Operators must factor varying RTP requirements and regulatory costs into provider selection and content placement strategies.

According to SOFTSWISS.