Nigeria's sports betting market has emerged from regulatory chaos with a clearer dual-track licensing framework, offering operators strategic choices between multi-state coverage and targeted regional entry. The transformation from a single federal authority to state-by-state fragmentation and finally to the current hybrid model reflects the challenges of governing Africa's most populous gambling market.

With a betting participation rate exceeding 71% and over 242 million citizens, Nigeria presents compelling opportunities despite regulatory complexity. The market's evolution through three distinct phases since 2005 has created today's landscape where operators can pursue either state-specific licenses or unified multi-state coverage through the Universal Reciprocity Certificate (URC) system.

The Regulatory Evolution: From Unity to Fragmentation to Consolidation

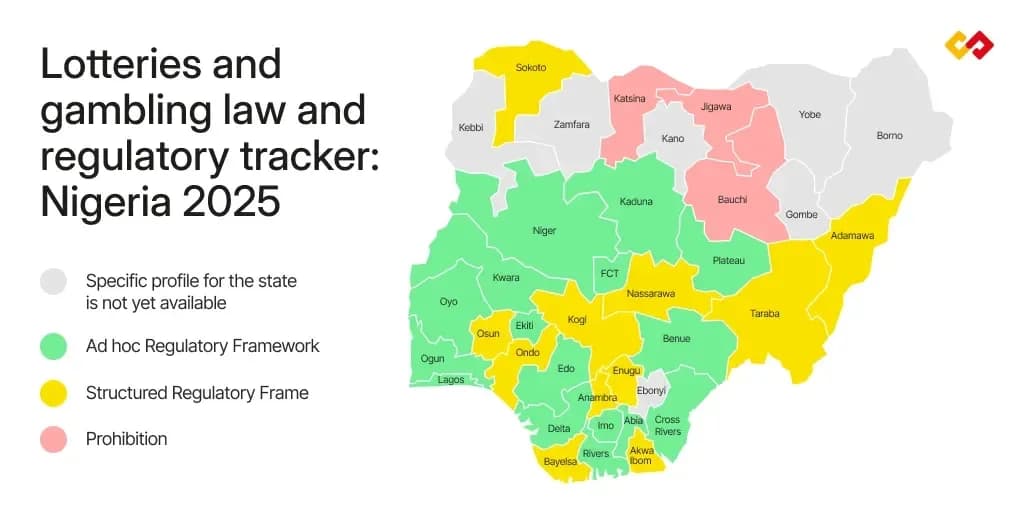

Nigeria's sports betting regulation has undergone dramatic restructuring, creating uncertainty before settling into the current dual-pathway system. The country's 36 states gained increasing autonomy over gambling regulation, fundamentally altering how operators approach market entry.

Federal Monopoly Period (2005 – 2024)

During this extended period, the National Lottery Regulatory Commission (NLRC) held exclusive authority under the National Lottery Act of 2005. Operators secured a single federal-level licence enabling nationwide sports betting services across all states. This centralised approach provided regulatory clarity but limited state-level customisation of gambling policies.

State-by-State Fragmentation (2024 – 2025)

The regulatory landscape shifted dramatically when the Supreme Court abolished the National Lottery Act of 2005 in November 2024. This decision restricted NLRC authority to the Federal Capital Territory, including Abuja, while granting all other states exclusive jurisdiction over gambling within their borders.

The immediate consequence forced operators to obtain separate licences for each target state rather than relying on nationwide coverage. This fragmentation created compliance burdens and overlapping tax obligations that complicated multi-state operations.

Current Multi-State Framework (2025 – Present)

Recognising operator confusion and administrative inefficiency, the Federation of State Gaming Regulators of Nigeria (FSGRN) established a unified framework among member states. The organisation introduced the Universal Reciprocity Certificate (URC), functioning as a mutually recognised licence across participating jurisdictions.

As of April 2026, 25 states participate in the FSGRN framework, enabling URC holders to offer betting services across this substantial coverage area. Non-member states require separate licensing arrangements, though operators can combine URC coverage with individual state licences for comprehensive market access.

FSGRN Membership Benefits

The Federation of State Gaming Regulators of Nigeria operates as a voluntary consortium, meaning states can join or withdraw at their discretion. Current non-member states include several northern jurisdictions and some southeastern states that prefer maintaining independent regulatory frameworks. Operators should verify current FSGRN membership before committing to URC applications, as membership changes can affect coverage areas.

Market Fundamentals: Demographics and Betting Behaviour

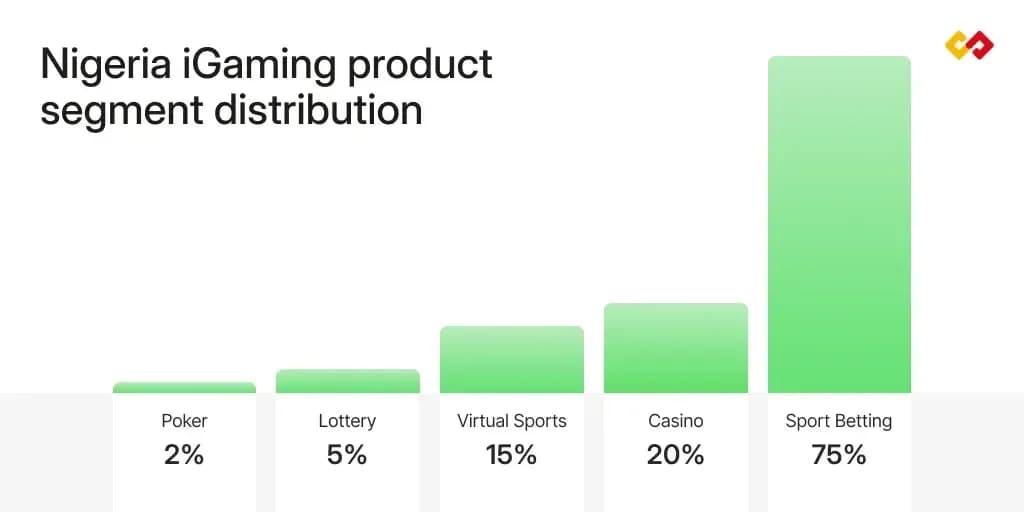

Nigeria's sports betting market combines demographic advantages with established gambling culture. Over 60% of the population is under 30, creating a digitally native audience aligned with online betting platforms. 25% of adults gamble daily, generating approximately $5.5 million (€4.7 million) in overall spending, with sports betting representing 75% of all wagers.

Geographic concentration favours major urban centres, with Lagos accounting for over 40% of players, alongside significant populations in Port Harcourt and Abuja. This concentration aligns with infrastructure development and disposable income distribution across the country.

Player behaviour reflects mobile-first preferences, with 93% of bets placed online and over 90% of users accessing the internet through mobile devices. This digital preference eliminates the need for extensive brick-and-mortar infrastructure, reducing operational overhead for new entrants.

Sports Preferences and Betting Patterns

Football dominates Nigerian sports betting, comprising 85% of total wagering activity. Domestic leagues including the Nigeria Premier Football League, Nigeria National League, and NWFL Premiership attract substantial interest alongside European competitions such as the English Premier League, UEFA Champions League, and La Liga.

Seasonal variations create predictable volume spikes during football seasons, enabling operators to optimise marketing spend and promotional activities. Other popular sports include basketball, tennis, boxing, athletics, and esports, though none approach football's market dominance.

Nigerian bettors typically place small stakes up to ₦500 (approximately $0.25 or equivalent) throughout the day, suggesting risk-averse behaviour focused on frequent, low-stakes engagement rather than occasional large wagers. Over 80% of players respond positively to bonuses and loyalty programmes, making retention incentives crucial for competitive differentiation.

Market projections indicate continued growth with a forecast CAGR of 6.92% by 2028, driven by expanding internet penetration, smartphone adoption, and deepening sports engagement across younger demographics.

Seasonal Marketing Optimization

Nigerian football seasons create distinct betting volume patterns that smart operators exploit. The Nigeria Premier Football League runs February to July, while European leagues operate August to May, creating year-round opportunities. Plan marketing budgets to coincide with UEFA Champions League knockout stages and English Premier League title races, when Nigerian engagement peaks by up to 300% compared to off-season periods.

242 million

Total Nigerian citizens

71%

Betting participation rate

60%

Population under 30 years

25%

Adults who gamble daily

$5.5 million

Annual gambling spending

75%

Sports betting share of wagering

40%

Lagos player concentration

93%

Online bet placement rate

90%

Mobile internet usage

85%

Football betting dominance

₦500

Typical maximum stake

80%

Players responding to bonuses

6.92%

Forecast CAGR by 2028

Licensing Pathways: Strategic Choices for Market Entry

The current regulatory framework offers two distinct licensing approaches, each serving different operational strategies and market objectives. Operators must evaluate coverage requirements, financial resources, and compliance capacity when selecting their preferred pathway.

State-Issued Licensing

State-specific licences grant exclusive operating rights within individual jurisdictions. This approach suits operators targeting high-value regions or testing market viability before broader expansion. Each state maintains its own regulatory authority with varying requirements and fee structures.

Key state regulators include the Lagos State Lottery and Gaming Authority for Nigeria's commercial capital and the Cross River State Lottery and Gaming Agency for southeastern markets. Lagos represents the largest player concentration, making its licence particularly valuable despite higher costs.

Universal Reciprocity Certificate (URC)

The URC provides standardised licensing across 25 FSGRN member states, eliminating the need for multiple applications and compliance frameworks. This unified approach reduces administrative burden while enabling broad market coverage through a single regulatory relationship.

However, Northern Nigerian states present particular challenges due to Sharia law restrictions on gambling activities. These jurisdictions maintain varying approaches from complete prohibition to regulatory uncertainty, requiring careful legal assessment before market entry attempts.

| Licence type | State-issued licence | Universal Reciprocity Certificate (URC) |

|---|---|---|

| Description | A licence granted by a specific state's regulatory authority that permits a sportsbook to operate exclusively within that state | A unified licence issued by the FSGRN that allows sportsbooks to operate across 25 member states |

| Best for | Sportsbook businesses planning to offer products within a single target state. Also an option if a target state is not an FSGRN member | Sportsbook businesses seeking multi-state reach |

| Regulatory authority | Each state has individual authority:<br>• Lagos State Lottery and Gaming Authority<br>• Cross River State Lottery and Gaming Agency | Federation of State Gaming Regulators of Nigeria |

| Application fee | €315 (Lagos example, varies by state) | €3,146 |

| Licence fee | €31,460 (Lagos) | €62,913 |

| Annual renewal | €6,290 (Lagos) | Not disclosed |

| Minimum capital | €12,552 (Lagos) | €62,761 |

Pros

- URC covers 25 states with single application process

- State licenses offer lower entry costs for testing markets

- Lagos state license provides access to 40% of player base

- URC eliminates multiple compliance frameworks

Cons

- URC requires higher minimum capital (€62,761 vs €12,552)

- Northern states remain largely inaccessible due to Sharia restrictions

- State-specific licenses limit expansion without additional applications

- FSGRN membership can change, affecting URC coverage

Licensing Requirements and Costs

Both licensing pathways follow similar application processes with documentation requirements covering business operations, financial capacity, technical infrastructure, and compliance systems. The minimum legal age for sports betting participation is 18 across all jurisdictions.

Lagos State Licensing Costs

For Nigeria's most valuable market:

- Non-refundable application fee: €315

- Licence fee: €31,460

- Annual renewal fee: €6,290

- Minimum share capital requirement: €12,552

Universal Reciprocity Certificate Costs

For multi-state coverage:

- Non-refundable application fee: €3,146

- Licence fee: €62,913

- Minimum share capital requirement: €62,761

- Renewal fees: not publicly disclosed

Application Process Timeline

Regulatory due diligence typically requires 10 – 15 working days for initial review. Successful applications receive a temporary Approval in Principle (AIP) licence valid for 90 days, during which operators must fulfil all conditions to obtain the substantive licence.

Required documentation includes:

Business Proposal: Operations structure, management hierarchy, marketing strategy, and KPI projections Financial Information: Account statements, tax clearances, capital investment sources, profit projections, and bank guarantees Sports Betting Operations: Covered sports, game frequency, odds mechanisms, and prize structures Technical Infrastructure: Architectural diagrams, hosting arrangements, server specifications, database systems Certifications: ISO 9001:2015 certificates, Gaming Laboratories International (GLI) or BMM Test certificates, Special Control Unit Against Money Laundering (SCUML) certificates

Both domestic and foreign businesses are eligible for Nigerian sports betting licences, provided they demonstrate proper business incorporation and meet capitalisation requirements.

Warning

The 90-day Approval in Principle period is non-negotiable and cannot be extended under current regulations. Operators failing to meet all conditions within this timeframe must restart the entire application process, including paying new application fees. Common compliance delays include incomplete SCUML certification, inadequate server infrastructure documentation, and insufficient responsible gambling system implementation.

Tax Framework: Simplification and Compliance

Nigeria's fiscal approach to sports betting has undergone significant simplification. From January 2026, staking amounts became VAT-exempt across all gaming verticals, eliminating the previous 7.5% VAT burden on player stakes. However, VAT continues applying to platform services, commission expenses, and operational costs.

Player winnings remain subject to withholding tax at state-determined rates, typically 5% for residents and 15% for non-residents. Additional state-specific levies may apply, such as Lagos's 2.5% tax on sales revenue or Oyo's 5% tax on turnover.

URC operators face an 11% tax on Gross Gaming Revenue regardless of gambling category, providing predictable fiscal obligations across member states. Company Income Tax applies at 30% for businesses exceeding ₦50M turnover, while smaller operators qualify for 0% CIT rates.

VAT Exemption Scope

The January 2026 VAT exemption specifically applies to player stakes but excludes affiliated services. Marketing expenses, payment processing fees, software licensing costs, and third-party integrations remain subject to standard VAT rates. This distinction requires careful accounting separation between gaming and non-gaming revenue streams for accurate tax reporting.

Payment Infrastructure: Local Solutions Drive Adoption

Nigerian bettors strongly favour domestic payment solutions over international alternatives, creating opportunities for operators who integrate local financial services effectively. The Nigeria Inter-Bank Settlement System (NIBSS) supports instant, secure interbank operations through NIBSS Instant Payments (NIP), recognised as Africa's first mature instant payment system.

Card and Banking Solutions

Visa and Mastercard enjoy widespread acceptance alongside Verve, the African domestic card brand. Bank transfers remain popular due to NIBSS infrastructure enabling real-time transactions with low consumer costs and strong governance frameworks.

Unstructured Supplementary Service Data (USSD) enables mobile payments using short symbolic-numeric codes, functioning offline to serve rural regions with unstable internet connectivity. This accessibility expands market reach beyond urban centres with reliable broadband infrastructure.

Leading payment gateways include Paystack, Flutterwave, Moniepoint, and Interswitch, offering API-driven integration for cards, bank transfers, USSD, and additional local methods.

Mobile Payment Leadership

Mobile solutions lead Nigeria's fintech market, with OPay and PalmPay providing fastest processing speeds and market leadership. Paga and Quickteller offer additional options, though international e-wallets like PayPal and Skrill face regional and compliance restrictions limiting adoption.

Cryptocurrency Potential

Nigeria demonstrates exceptional cryptocurrency adoption, with 84% of citizens owning crypto wallets and 74% having purchased cryptocurrency according to 2024 surveys. Bitcoin, Binance Coin, and Ethereum represent the most widely owned and traded cryptocurrencies, presenting opportunities for crypto sportsbook operators targeting this digitally advanced population.

Regulatory Uncertainty Warning

Despite Nigeria's exceptional crypto adoption rates, the Central Bank of Nigeria maintains restrictive policies toward cryptocurrency transactions. While citizens own crypto wallets, direct crypto-to-naira conversions through traditional banking remain prohibited. Operators considering crypto payments must implement third-party conversion services and ensure compliance with evolving financial regulations that could change rapidly.

Technology Platform Selection: Custom vs Turnkey Solutions

Sportsbook software selection represents both technical and strategic business decisions affecting time-to-market, customisation capabilities, and long-term operational flexibility. Operators must balance development costs, launch timelines, and competitive differentiation requirements.

Custom Sportsbook Development

Custom platforms offer unlimited customisation and proprietary ownership, enabling unique interfaces, incentive mechanisms, odds integrations, and payment services. However, development requires substantial upfront investment with delayed ROI realisation, often extending launch timelines to months or over a year.

The Time and Material contract approach creates unpredictable costs while requiring in-house technical teams or external contractors for ongoing support. Mid- to long-term ROI perspectives may justify these investments for operators with substantial resources and specific differentiation strategies.

Turnkey Sportsbook Solutions

Turnkey platforms provide preconfigured solutions with customisation and branding capabilities, enabling operators to launch functional sportsbooks within weeks rather than months. Lower upfront costs and predictable pricing structures accelerate break-even timelines while reducing technical complexity.

Back office functionality enables flexible adjustment of sports offerings, bonus structures, localisation, and operational parameters. Customisable frontends maintain brand alignment while leveraging proven technical infrastructure. Integration compatibility with casino solutions expands product portfolios efficiently.

The SOFTSWISS Sportsbook Platform exemplifies turnkey solutions offering granular CMS customisation, flexible gamification scenarios, reliable odds provider integration, and 14 – 30 day launch timelines for competitive market entry.

| Factor | Custom Sportsbook | Turnkey Sportsbook |

|---|---|---|

| Time-to-market | Launch in months, sometimes 1+ year | Launch in weeks |

| Initial investment | High and often unpredictable upfront costs due to Time and Material contracts | Lower upfront costs, predictable pricing |

| Customisation | Unlimited and fully controlled by the operator | From medium to granular, depending on the provider |

| Operational complexity | High and requires in-house team or external contractor for post-release support | Low and supported by the provider before and after release |

| ROI timeline | Mid- to long-term perspective | Short- to mid-term perspective |

How to Evaluate Sportsbook Platform Options

Define Technical Requirements

List essential features including payment methods, odds providers, mobile optimization, and integration capabilities with existing systems

Calculate Total Cost of Ownership

Include development costs, ongoing maintenance, hosting fees, compliance updates, and technical support over 3-5 years

Assess Time-to-Market Impact

Evaluate revenue loss from delayed launches against customization benefits, considering competitive positioning

Verify Regulatory Compliance

Ensure platforms include KYC, AML, responsible gambling tools, and Nigerian-specific reporting capabilities

Test Integration Capabilities

Confirm compatibility with Nigerian payment providers, local banks, and required compliance systems before final selection

Essential Platform Features

Successful sportsbook operations require comprehensive feature sets addressing player management, content customisation, payment processing, and regulatory compliance. Core functionality includes:

Player Account Management (PAM): KYC compliance through data collection, storage, and customer management Content Management System (CMS): Website and application content control for text, visuals, and layouts Payment Processing: Multiple method support including cards, bank transfers, fintech apps, e-wallets, and cryptocurrency Odds Provider Integration: Trustworthy betting odds from established data suppliers Sporting Events Coverage: Diverse sports offerings to expand audience reach and increase net gaming revenue Analytics and Reporting: KPI tracking and stakeholder transparency Gamification: Bonus systems, loyalty programmes, tournaments, and jackpots for player engagement Fraud Prevention: Account restrictions, additional verification checks, and operator alerts Customer Support: Omnichannel request management and accelerated issue resolution

Success in Nigeria's crowded sportsbook market requires more than just meeting regulatory minimums – operators must deliver superior mobile experiences, local payment integration, and culturally relevant content to compete against established players holding 85% market share.

Regulatory Compliance: Non-Negotiable Prerequisites

Federation of State Gaming Regulators of Nigeria

Responsible gambling and regulatory compliance represent mandatory operational requirements rather than optional features. These frameworks protect both players and operators through structured risk management approaches.

Responsible Gambling Implementation

Responsible gambling prevents gambling disorder through impulse control mechanisms:

- Wager, deposit, and loss limits

- Reality checks for continued play verification

- Cooling-off periods for temporary access restriction

- Self-exclusion options for extended account suspension

Compliance Procedures

Regulatory compliance ensures all stakeholders operate within Nigerian legal frameworks: Know Your Customer (KYC): Identity verification through ID requests, address proof, liveness checks, and biometric verification Anti-Money Laundering (AML): Transaction monitoring and suspicious activity reporting

Compliance adherence protects brand reputation while enabling players to enjoy betting entertainment within appropriate boundaries.

Go-to-Market Strategy: Launch Roadmap

Successful Nigerian market entry requires systematic execution across regulatory, technical, and marketing domains. The structured approach includes:

- Business Registration: Incorporate with the Corporate Affairs Commission (CAC) to obtain legal entity status, Tax Identification Number (TIN), and Nigerian bank account

- Licence Acquisition: Choose between state-specific licensing for targeted regions or URC for multi-state coverage across 25 member states

- Technology Deployment: Implement custom or turnkey sportsbook solutions, potentially integrating with existing casino platforms for comprehensive player experiences

- Payment Integration: Enable popular local payment methods through partnerships with Nigerian banks and payment solution providers

- Marketing Launch: Execute promotional campaigns aligned with regional player profiles and regulatory requirements

Marketing and Promotion: Regulatory Compliance Framework

Nigeria offers substantial promotional opportunities for sports betting operators willing to navigate federal and state-level advertising regulations. The Advertising Regulatory Council of Nigeria (ARCON) provides federal oversight while state gambling authorities maintain jurisdiction-specific requirements.

Recent regulatory harmonisation occurred when ARCU partnered with FSGRN, signing a memorandum of understanding effective 1 April 2026 to unify advertising rules across member states. This agreement reduces compliance complexity for multi-state operators, though specific stipulations require direct regulatory consultation.

Available Marketing Channels

Promotional channels include television, radio, print media, online platforms, and social networks. Meta products including WhatsApp, Facebook, and Instagram lead social media engagement alongside TikTok and Telegram. Google's 2025 reversal of its gambling advertising ban created additional SEO and PPC opportunities for compliant operators.

Affiliate marketing deserves particular attention for its performance-based model combining broad reach with targeted traffic. Media partnerships, influencer collaborations, community engagement, brand partnerships, and online platform integration enable bookmakers to attract and pay only for qualified conversions.

Centralised affiliate management through iGaming software platforms enables performance analysis, traffic criteria establishment, commission adjustment, and streamlined payment processing under unified administrative control.

Compliance Requirements

Marketing strategies must promote responsible gambling while avoiding prohibited practices including:

- Minor targeting or vulnerable individual exploitation

- Exaggerated winning probability claims

- Easy earning emphasis or unrealistic income promises

Market Competition and Differentiation

Nigeria's established sports betting market features over 40 active operators competing for market share. Bet9ja leads with an estimated 35 – 40% market share, followed by BetKing (20 – 25%), SportyBet (15 – 20%), Betway (10%), and 1xBet (5 – 10%).

New entrants must differentiate through superior user experience, competitive odds, attractive bonus structures, or innovative features addressing unmet player needs. Feature-rich platforms with versatile bonus options provide competitive advantages in this saturated market environment.

Regional Considerations: Northern State Restrictions

Northern Nigerian states present unique challenges due to Sharia law influence on gambling regulation. These jurisdictions maintain varying approaches from complete prohibition to regulatory uncertainty, requiring careful legal assessment before market entry attempts.

Secular constitutional provisions coexist with Islamic legal principles creating complex regulatory environments where gambling may contradict religious teachings. Operators should evaluate these restrictions when determining market coverage strategies and resource allocation priorities.

Financial Projections and Market Opportunity

Nigerian gambling generated $3.86 billion in annual revenue during 2025, with sports betting representing 75% of total wagering activity. Over 25% of adults participate in gambling, with the majority focusing on sports events rather than casino or lottery products.

The online sports betting market continues expanding with technological advancement, increasing smartphone penetration, and deepening sports engagement across younger demographics. Operators entering this market can leverage established demand, proven payment infrastructure, and regulatory clarity to build sustainable businesses.

Strategic Considerations for Market Entry

Nigeria's sports betting licensing transformation from regulatory chaos to structured dual-pathway system creates clearer market entry strategies for domestic and international operators. The Universal Reciprocity Certificate enables efficient multi-state expansion while state-specific licensing allows targeted regional focus with lower initial investment requirements.

Success in this market demands understanding of local player preferences, payment method integration, mobile-first platform design, and compliance with responsible gambling requirements. Football-centric content strategies, small-stake betting accommodation, and bonus-sensitive player engagement represent crucial competitive factors.

The regulatory environment continues evolving toward greater streamlining and operator accessibility, suggesting favourable long-term prospects for well-positioned market entrants. However, established competition requires differentiated value propositions and superior execution to achieve meaningful market penetration and sustainable profitability.

Yes, both domestic and foreign businesses can apply for Nigerian licenses independently, provided they meet incorporation requirements with the Corporate Affairs Commission. However, local partnerships often accelerate payment integration and regulatory navigation.

URC coverage automatically ends in withdrawn states, requiring separate state license applications to continue operations. Operators should monitor FSGRN membership changes and maintain contingency licensing strategies for key markets.

Northern states maintain varying approaches from complete gambling prohibition to regulatory uncertainty due to Islamic law influence. Operators must conduct state-by-state legal assessments and avoid marketing in prohibited jurisdictions to prevent regulatory violations.

While 84% of Nigerians own crypto wallets, Central Bank restrictions limit direct crypto-naira conversions through traditional banking. Operators can implement crypto payments through compliant third-party conversion services, though regulatory uncertainty remains.

Common rejection factors include insufficient minimum capital, incomplete technical documentation, missing ISO certifications, inadequate responsible gambling systems, and failure to demonstrate proper AML compliance procedures. Thorough preparation prevents most rejections.

According to SOFTSWISS.