South Africa's sports betting market presents a compelling entry opportunity for international operators seeking exposure to Africa's most established gambling jurisdiction. With €76 billion in wagering turnover and €3.8 billion in gross gaming revenue recorded in FY2024/25, the market combines regulatory maturity with substantial scale – a combination rarely found across the continent.

The country has been regulating sports betting since 1996, creating nearly three decades of settled law and competitive infrastructure. Online betting now drives 60% of the betting market revenue, reflecting a digitally sophisticated bettor base with 81% smartphone penetration rates.

Provincial Licensing Framework Determines Market Access

Operating without a valid provincial licence constitutes a criminal offence under South African law, with personal liability extending to directors and key employees. The National Gambling Act 2004 establishes the legislative framework, while nine Provincial Licensing Authorities handle day-to-day compliance oversight.

A single provincial licence provides nationwide online betting authorization, but application timelines stretch six to nine months. Several high-value provinces have closed their licensing books, forcing new entrants to evaluate remaining jurisdictions carefully.

Three licence categories govern market participation:

- Bookmaker licence – Core commercial authorization for accepting public wagers

- Key employee licence – Individual approval required for executives and compliance officers

- Bookmaker premises licence – Covers registered operational addresses

The National Gambling Board provides overall regulatory coordination, ensuring consistent standards across provincial boundaries. However, each Provincial Licensing Authority maintains independent application processes and fee structures.

Warning

Directors and key employees face personal criminal charges for unlicensed operations. South African courts have prosecuted international executives who operated without provincial authorization, with penalties including fines up to R10 million and imprisonment terms.

Market Concentration Creates Strategic Opportunities

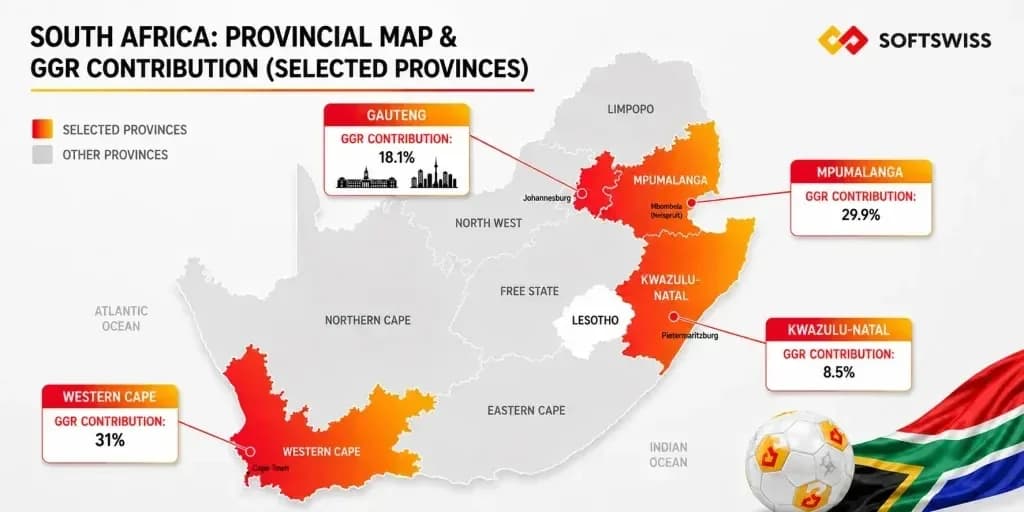

National Gambling Board reported data reveals significant geographical concentration within South Africa's betting market. Western Cape commands 31% of total GGR, Mpumalanga holds 29.9%, and Gauteng contributes 18.1% – three provinces accounting for 79% of national revenue. KwaZulu-Natal adds another 8.5%, creating clear targeting priorities for new operators.

More than 50 licensed operators compete in South Africa, but revenue consolidation occurs around a much smaller group. Betway maintains national coverage focusing on soccer, rugby, and cricket. Hollywoodbets leverages retail-online hybrid models with particular strength in KwaZulu-Natal. Bet.co.za emphasizes local brand identity across Gauteng markets, while Supabets pursues price-focused positioning in Gauteng and Western Cape.

According to GeoPoll's 2025 Betting in Africa survey, 83% of South African respondents had placed bets within the past year – the highest participation rate continent-wide, exceeding Kenya (79%), Tanzania (74%), and Nigeria (73%).

| Operator | Primary Sports | Mobile App | Notable Differentiator | Provincial Focus |

|---|---|---|---|---|

| Betway | Soccer, rugby, cricket | Yes | Global brand, broad market depth | National |

| Hollywoodbets | Horse racing, soccer | Yes | Retail + online hybrid, loyalty programme | KwaZulu-Natal, national |

| Bet.co.za | Soccer, cricket | Yes | Local brand identity, competitive odds | Gauteng, national |

| Supabets | Soccer, basketball | Yes | Price-focused positioning, eSports coverage | Gauteng, Western Cape |

€76 billion

Annual wagering turnover

€3.8 billion

Gross gaming revenue FY2024/25

60%

Online betting market share

81%

Smartphone penetration

31%

Western Cape GGR share

29.9%

Mpumalanga GGR share

83%

South African betting participation rate

Technology Platform Selection Drives Market Timeline

Platform architecture represents the most consequential technology decision for new market entrants. Two primary development paths exist: turnkey solutions and proprietary builds, each carrying distinct cost and timeline implications.

Turnkey solutions offer 3 – 6 months to market launch with moderate capital requirements. These platforms provide operator-controlled instances with significant customization capabilities while leveraging provider-maintained infrastructure.

Proprietary development demands €920K – €2.76M+ in initial investment with 12 – 24 months development timelines. While offering complete product control, proprietary builds require substantial technical teams and extended pre-revenue periods.

SOFTSWISS Market Integration

SOFTSWISS Sportsbook holds WCGRB licensing as a B2B provider with GLI South Africa certification. This regulatory pre-approval eliminates technical audit delays that typically extend South African market entry timelines by several months.

The platform delivers native ZAR support, pre-built API integration with data feeds and KYC tools, plus SaaS delivery models that maintain infrastructure management with the provider during initial operations. Modular architecture supports incremental feature activation, while validated scalability handles high-concurrency traffic loads.

| Factor | Turnkey | Proprietary |

|---|---|---|

| Cost | Moderate capital expenditure; predictable fee structure | High development costs (€920K – €2.76M+) |

| Time to Market | Fast (3 – 6 months) | Slowest (12 – 24+ months) |

| Customisation | Significant – operator-owned instance, configurable to brand and market | Full control – but every feature demands internal resources |

| Scalability | High – provider-maintained infrastructure scales with your growth | Unlimited, but entirely resource-intensive |

| Control | Strong – operator owns the product roadmap within a proven framework | Complete – but carries full technical and compliance risk |

Development Budget Reality Check

Industry analysis shows 70% of operators attempting proprietary builds exceed initial budgets by 40-60% and miss launch deadlines by 6-12 months. Factor in recurring costs for security patches, feature updates, and compliance modifications when calculating total ownership expenses.

Payment Infrastructure Reflects Mobile-First Reality

South Africa's payment landscape serves a partially unbanked, mobile-native population requiring specialized integration strategies. Smartphone penetration at 81% makes mobile-first design non-negotiable for competitive positioning.

Essential payment method categories include:

- Mobile payments – EFT via mobile banking applications

- Credit and debit cards – Visa and Mastercard for urban depositors

- E-wallets – Skrill, Neteller, and localized options

- Cryptocurrency – Bitcoin, Ethereum, and stablecoins for borderless transactions

All transactions must process in South African Rand (ZAR) to build bettor confidence. Fast payouts and instant withdrawals serve as primary retention mechanisms in competitive markets.

Multiple payment service provider integration ensures failover routing capabilities. SSL encryption, PCI-DSS alignment, and comprehensive fraud prevention protocols must cover all transaction touchpoints.

Banking Partnership Requirements

South African banks require gambling operators to maintain dedicated merchant accounts with enhanced monitoring. Standard approval timelines run 4-8 weeks, but some banks blacklist gambling transactions entirely. Secure backup banking relationships before launch to avoid payment disruptions.

Sports Content Strategy Reflects Local Preferences

Market-specific sports content drives acquisition and retention across South African betting platforms. Rugby featuring the Springboks generates peak traffic volumes, while soccer delivers highest daily betting volume. Cricket shows strong seasonal demand patterns.

Horse racing operates through distinct institutional frameworks involving Gold Circle and Phumelela for totalisator systems and on-course relationships. The Kenilworth Racing Trust represents Western Cape racing interests. Any operator adding horse racing must understand these institutional relationships with provincial regulators.

Essential betting market categories by sport:

| Sport | Betting Types | Market Notes |

|---|---|---|

| Rugby (Springboks) | Pre-match, in-live, proposition | Peak traffic driver |

| Soccer | Pre-match, in-live, bet builder | Highest daily volume |

| Cricket | Pre-match, in-live | Strong seasonal demand |

| Horse racing | Pre-match, tote | Distinct institutional framework |

| Basketball | Pre-match, in-live | Urban youth market |

| eSports | Pre-match, in-live | Fast-growing younger demographic |

In-live betting and bet builder functionality represent the highest-margin product enhancements available post-launch.

Rugby Premium Content Access

SuperSport holds exclusive broadcasting rights for most Springboks matches and domestic competitions. Operators seeking premium rugby content must negotiate separate data licensing agreements, with costs ranging R500,000-R2 million annually depending on coverage scope.

Compliance Framework Requires Integrated Architecture

South African gambling compliance extends far beyond licence approval. AML, KYC, POPIA, and responsible gambling obligations face active monitoring by provincial boards throughout operations.

The Financial Intelligence Centre Act 38 of 2001 designates licensed operators as accountable institutions requiring comprehensive anti-money laundering controls. KYC procedures must include identity verification at registration, address verification above defined transaction thresholds, and ongoing transaction monitoring for suspicious patterns.

Mandatory responsible gambling tools include self-exclusion capabilities, deposit and betting limits, reality checks, and direct links to problem gambling support services. These systems share infrastructure with operational risk controls including exposure limits per event and liability tracking dashboards.

Cybersecurity obligations mandate SSL encryption across all data touchpoints. Gambling advertising laws require responsible gambling warnings in all communications, National Responsible Gambling Programme helpline references, and 18+ participation statements.

How to Implement AML Compliance Architecture

Customer Risk Assessment

Deploy automated screening against OFAC, UN, and EU sanctions lists at registration with ongoing monitoring for PEP status changes

Transaction Monitoring Setup

Configure real-time alerts for deposits exceeding R25,000, rapid-fire betting patterns, and unusual withdrawal requests requiring manual review

Suspicious Activity Reporting

Establish direct FIC reporting channels with 15-day STR filing requirements and designated compliance officer authorization protocols

Record Keeping Systems

Maintain 5-year customer transaction histories with encrypted storage and audit trail capabilities for regulatory inspections

Sports Data Integration Powers Real-Time Operations

Sports data APIs and live feeds enable every betting market from pre-match lines to in-live wagering and bet builder functionality. Odds management depends entirely on feed quality, with margin protection and settlement accuracy requiring precise, timely data delivery.

Critical evaluation criteria for data providers include low latency performance (delays exceeding 3 seconds create arbitrage opportunities in in-live betting), comprehensive data integrity across event creation and settlement processes, broad event coverage for South African and global markets, and betting automation capabilities for line movements and result settlement.

Annual costs for full-coverage sports data feeds range €129,000 – €438,600, representing significant ongoing operational expenses that must be factored into cash flow projections.

Data Feed Redundancy Strategy

Major sports betting outages during Springboks matches cost operators an average of R2.3 million per hour in lost revenue. Primary data providers include Sportradar, Betradar, and LSports, but smart operators maintain secondary feeds from different providers to ensure continuous operations during technical failures.

Marketing Strategy Within Regulatory Constraints

Gambling advertising laws under the National Gambling Act 2004 require responsible gambling warnings, National Responsible Gambling Programme helpline information, and 18+ participation statements across all marketing communications.

In markets where Betway and Hollywoodbets maintain national brand recognition, new operators require clear positioning statements and unique value propositions before committing channel investments.

Primary acquisition channels include affiliate marketing (most capital-efficient option via revenue share or CPA structures), SEO for high-intent organic visibility, local club sponsorships offering strong ROI for new brands, and programmatic display advertising for betting-intent audiences.

Retention strategies focus on deposit bonuses and free bet welcome offers as industry baseline requirements, cashback programs to reduce churn following losing streaks, VIP memberships with loyalty rewards for high-value players, and gamification mechanics including tournaments and leaderboards to sustain engagement between major sporting events.

Financial Planning for Market Entry

Comprehensive startup cost analysis reveals multiple expense categories extending beyond headline licensing fees:

| Category | Cost Range (EUR) | Frequency |

|---|---|---|

| Licensing | €712 – €25,800+ | One-time + annual |

| Technology | €185,800 – €2.37M+ | One-time + recurring |

| Operations | €1,860 – €14,190/month | Recurring |

| Staffing | €14,190 – €77,400/month | Recurring |

| Infrastructure | €1,390 – €9,440/month | Recurring |

| Marketing | €18,890 – €94,430+ | Recurring |

| Compliance | €4,720 – €28,380/year | Recurring |

Hidden costs including maintenance, patches, and overhead expenses accumulate before first-bet revenue generation. A 20% contingency reserve provides essential financial buffer during pre-revenue operations.

Proprietary development costs reach €872K – €2.62M with 18 – 24 month realistic build timelines, making turnkey solutions more practical for most new market entrants.

South African tax obligations include GGR-based levies, VAT, and corporate tax on profits, plus payroll and PAYE requirements beginning with first employee hires. Cash flow planning between licence approval and meaningful revenue generation represents the most critical financial discipline for new operators.

The gap between licensing approval and meaningful revenue generation represents the biggest financial risk for new South African operators, with most requiring 8-12 months of operational funding before achieving positive cash flow.

Growth Trajectory Analysis

34% between 2020 and 2025 reveals 34% compound annual growth rates between 2020 and 2025, moderating to 26% subsequently. Online betting contributed approximately €2.6 billion to total regulated gambling GGR – representing 70% of the market segment.

This growth trajectory positions South Africa as the continent's most attractive regulated betting market, combining established infrastructure with continued expansion potential. The regulatory framework provides operational stability while digital adoption trends support long-term revenue growth.

Strategic Market Entry Considerations

Provincial licensing remains the primary market access barrier, with application timelines stretching six to nine months and several high-value jurisdictions closing their books to new applicants. Early engagement with available Provincial Licensing Authorities becomes essential for realistic market entry planning.

Technology platform selection between turnkey and proprietary solutions determines both time-to-market and ongoing operational flexibility. For most operators, turnkey solutions offer optimal balance between speed and control, making them the preferred choice over resource-intensive proprietary development.

Compliance architecture must be designed as integrated systems rather than independent pillars. AML/KYC, responsible gambling, and cybersecurity share infrastructure and data requirements, making unified design approaches more practical and cost-effective.

Mobile-first design with 81% smartphone penetration makes responsive web and native app performance on mid-range Android devices absolutely essential for competitive positioning.

No, operating without a South African provincial license is a criminal offense. Offshore licenses provide no legal protection and expose operators and executives to prosecution.

Most provinces require 6-9 months for complete approval. Northern Cape and Free State typically process applications faster than Western Cape or Gauteng, but high-value provinces may be worth the wait.

Realistic minimum budgets start around €500,000 for turnkey solutions including licensing, platform costs, and 12 months operating expenses. Proprietary development requires €1.5-3 million minimum.

Yes, licensed operators must maintain registered premises within their licensing province. Virtual offices don't satisfy regulatory requirements, and compliance inspections occur without advance notice.

Most successful operators achieve break-even within 8-15 months post-launch, depending on marketing spend and customer acquisition efficiency. Premium provinces with established competition may require longer investment periods.

According to SOFTSWISS.