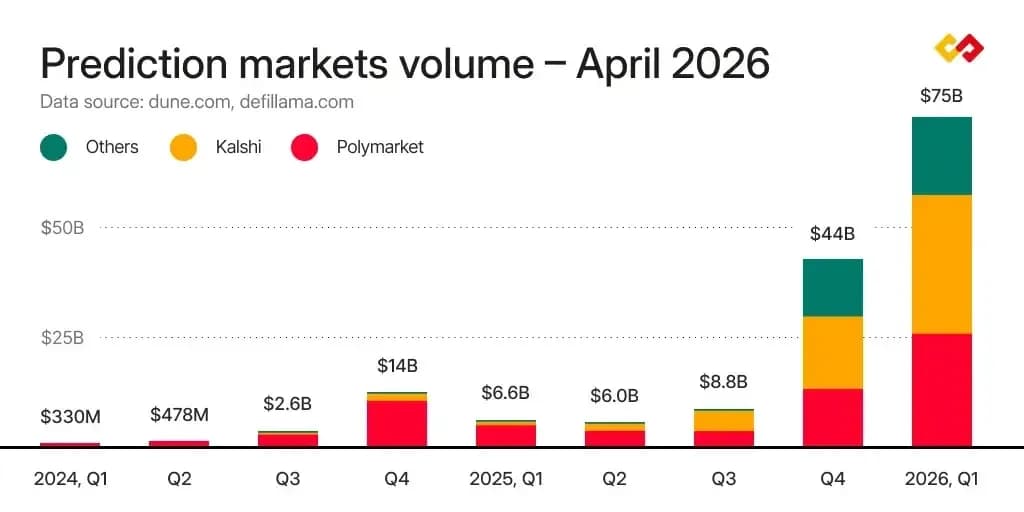

The prediction markets sector exploded into mainstream consciousness during 2025, transforming from a niche trading category into a $44 billion industry that has captured the attention of both regulators and iGaming operators worldwide. This surge followed the 2024 US elections, when platforms like Polymarket and Kalshi demonstrated that event-based trading could attract mass audiences far beyond traditional financial markets.

The mechanics are familiar to anyone running a sportsbook – participants place money on real-world outcomes and receive payouts if their predictions prove correct. The critical difference lies in scope: these platforms extend beyond sports into politics, economics, cultural events, and virtually any measurable future occurrence. For an industry constantly seeking new engagement verticals, this represents significant untapped potential.

Major US sportsbooks have already moved to capitalise on this opportunity. FanDuel and DraftKings have launched dedicated prediction market spin-offs, recognising the substantial overlap in customer demographics and betting behaviours. The question for other operators is no longer whether prediction markets belong in their ecosystem, but how quickly they can integrate them effectively.

Understanding Prediction Market Mechanics

Prediction markets operate as marketplaces where participants back their expectations about future events with real money. Events are typically structured as binary yes-or-no questions, with participants buying positions that pay out if their prediction proves accurate. Contract prices fluctuate based on trading activity, creating real-time probability assessments that often prove more accurate than traditional polling methods.

The concept has deeper roots than most industry professionals realise. Traders wagered on papal elections in 16th-century Europe, and by the early 1900s, Wall Street betting pools on US presidential races were common enough that the New York Times published their odds regularly. The internet era has simply democratised access and expanded the range of tradeable events.

Two platforms currently dominate the conversation. Polymarket, launched in 2020 and built on blockchain technology, operates as a decentralised exchange. Kalshi, live since 2021, functions as a centralised platform with traditional corporate oversight. Smaller players like PredictIt and Manifold operate on more focused scales, often targeting specific topics or communities, but are steadily growing their user bases.

The operational models divide into centralised and decentralised approaches. Centralised platforms like Kalshi manage user accounts, hold funds, and settle outcomes through traditional corporate structures. Decentralised markets use smart contracts to facilitate trading and payouts without central intermediaries, though this can create additional regulatory complexities.

$44 billion

Prediction markets industry value in 2025

$1

Standard contract payout amount

$0.65

Example contract price reflecting 65% probability

$0.35

Potential profit per share in example scenario

Peer-to-Peer Trading Dynamics

In the dominant peer-to-peer model, participants trade contracts directly with one another rather than against a house. Each contract represents a specific outcome and pays a fixed amount – typically $1 – if that outcome occurs. Contract prices range between $0 and $1, with the current price reflecting the market's collective probability assessment.

Consider a market asking: "Will country X enter a recession this year?" If "Yes" shares trade at $0.65, the market implies a 65% probability of recession. A participant believing recession is likely can buy "Yes" shares at $0.65. If recession occurs, each share settles at $1, generating $0.35 profit per share. If recession doesn't materialise, shares expire worthless.

Price movements reflect supply and demand dynamics. When more traders want to buy "Yes" shares than sell them, buyers must offer higher prices, pushing the contract price upward. Conversely, excess selling pressure drives prices down. This creates continuous price discovery as new information enters the market and participants adjust their positions accordingly.

The recession example illustrates another key feature: traders can exit positions early by selling contracts before resolution. If recession probability appears to increase, pushing "Yes" shares from $0.65 to $0.80, original buyers can sell for immediate profit without waiting for the final outcome. This differs significantly from traditional sportsbook cashout features, where operators set exit prices often at substantial discounts.

Contract Pricing Logic

Contract prices between $0 and $1 directly translate to percentage probabilities. A $0.40 contract implies 40% probability, while $0.85 suggests 85% likelihood. This mathematical relationship enables traders to quickly assess market sentiment and identify potential value opportunities.

Market Creation and Revenue Models

Each platform maintains dedicated teams responsible for researching, structuring, and launching new prediction markets. These teams define questions, establish clear resolution criteria, and objectively settle outcomes. Platforms also accept market suggestions from participants, though proposals undergo rigorous review processes before approval.

Three key principles guide market approval decisions. First, manipulation risk must remain minimal to ensure fair trading environments. Second, markets must not encourage harmful or unethical behaviour. Third, outcomes must rely on trusted, verifiable data sources. Only markets meeting these standards receive approval for trading.

Revenue generation typically occurs through transaction fees – small percentages charged on each trade. Some platforms may include fees on winnings or market creation activities. This model ensures sustainable operations while maintaining active, liquid markets that attract continued participation.

Revenue Optimization Strategy

Platforms maximize revenue by maintaining optimal transaction fee structures that balance profitability with trading volume. Higher fees reduce activity but increase per-trade revenue, while lower fees encourage volume. Most successful platforms settle around 1-2% transaction fees to maintain healthy liquidity.

Comparing Prediction Markets to Sports Betting

The structural differences between prediction markets and traditional sportsbooks are significant, despite surface-level similarities. Sportsbooks operate as centralised platforms where players bet against the house, which sets odds, applies margins, and manages all payouts. The focus remains largely on sporting events, though this has expanded to include in-game occurrences like total goals or individual player performance.

While sportsbooks offer early exit options through cashout features, operators determine these prices and typically include substantial margins that limit player returns. The house controls both entry and exit pricing, maintaining consistent profit margins across all betting activity.

Prediction markets function as peer-to-peer systems where participants trade directly with each other. Prices emerge dynamically through market forces rather than operator decisions. Participants can freely buy and sell contracts before event resolution, with exit prices determined by market demand rather than operator margins.

This fundamental difference creates opportunities for participants to profit through position trading rather than just outcome prediction. A trader might buy a contract at $0.40, sell it at $0.70 when sentiment shifts, and profit regardless of the final outcome. This dynamic trading element distinguishes prediction markets from static bet placement in traditional sportsbooks.

Pros

- Peer-to-peer trading eliminates house edge margins

- Dynamic exit pricing allows profit before event resolution

- Broader event coverage beyond sports entertainment

- Market-driven odds reflect true probability assessments

Cons

- More complex trading mechanics for casual users

- Liquidity issues in niche markets

- Higher regulatory uncertainty in many jurisdictions

- Requires sophisticated risk management systems

Global Regulatory Landscape

As of April 2025, no unified global approach exists for classifying and regulating prediction market platforms. Regulatory responses typically fall into three categories: financial instruments, gambling products, or undefined grey areas. This classification determines whether platforms can operate, face restrictions, or encounter outright bans in specific jurisdictions.

The United States treats prediction market platforms primarily as financial products. Kalshi operates under Commodity Futures Trading Commission (CFTC) regulation, though the regulatory environment continues evolving rapidly. In March 2025, US lawmakers introduced the Prediction Markets Are Gambling Act, which could fundamentally reclassify event trading as gambling rather than financial activity.

Europe lacks a unified approach, with individual countries applying their own frameworks. Most treat prediction markets as gambling platforms requiring appropriate licensing. Gibraltar became the first European jurisdiction to licence a prediction markets operator in 2026, granting approval to Predict Street as a betting intermediary under existing gambling regulations. The platform is set to launch with markets tied to the 2026 FIFA World Cup.

Regional Regulatory Classifications

North America presents a mixed picture. The US maintains partial regulation under financial frameworks, while Canada operates in a grey area. Prediction markets function across Canada except in Ontario, where they were banned in 2025. Canadian regulators may classify these platforms as securities, derivatives, or both.

European Union countries vary significantly in their approaches. Many nations including Belgium, France, Italy, Poland, and Romania have banned prediction market platforms as unlicensed gambling operations. The United Kingdom classifies them as betting platforms requiring Gambling Commission licences to operate legally.

Asia predominantly restricts prediction market access. Singapore has blocked platform access entirely, while Thailand is moving toward implementing restrictions. Most Asian countries treat these platforms as unlicensed gambling activities.

Oceania maintains restrictive positions. Australia bans prediction markets as unlicensed activities, while New Zealand prohibits them under existing gambling laws. Neither country shows signs of developing accommodating regulatory frameworks.

South America largely restricts or operates in grey areas. Argentina and Brazil have banned platforms as unlicensed operations. Chile and Peru maintain unclear regulatory positions, creating uncertainty for potential operators.

Africa lacks regulatory clarity across most jurisdictions, though focus is increasing as of early 2025. Limited frameworks exist, but growing platform popularity is prompting regulatory attention continent-wide.

Gibraltar Licensing Milestone

Gibraltar's 2026 approval of Predict Street as the first European licensed prediction market operator establishes important precedent. This licensing model under existing betting intermediary regulations may influence other EU jurisdictions considering similar frameworks.

Warning

The March 2025 Prediction Markets Are Gambling Act could fundamentally reshape US operations, potentially requiring existing platforms to obtain gambling licenses rather than financial regulatory approval. Operators should prepare contingency plans for rapid regulatory reclassification.

Fixed-Odds Implementation for iGaming Operators

While traditional exchange-based prediction markets require complex infrastructure including liquidity pools, matching engines, and fundamentally different risk frameworks, many operators prefer alternative implementations that align with existing operational models. Fixed-odds prediction markets represent one such approach that adapts core concepts to established sportsbook frameworks.

In fixed-odds models, players place bets directly against operators rather than trading with other participants. Odds derive from implied probabilities and adjust continuously based on market signals, exposure calculations, and risk management logic. However, once a bet is accepted, odds become fixed – consistent with standard sportsbook mechanics.

From a product perspective, this approach enables operators to expand beyond sports into politics, economics, and cultural events while maintaining familiar structural and commercial frameworks. Players understand the betting process, and operators can manage risk using existing tools and methodologies.

Operationally, fixed-odds models significantly lower barriers to entry. Integration typically occurs via API or iFrame deployment, allowing implementation within existing platforms without substantial development overhead. This accessibility makes prediction markets viable for operators who cannot justify building full exchange infrastructure.

Fixed-odds prediction markets allow operators to capture the engagement benefits of event-based trading while maintaining the risk management and operational simplicity of traditional sportsbook models.

The SOFTSWISS Prediction Markets platform exemplifies this approach, offering operators turnkey solutions that integrate event-based betting into existing ecosystems. This enables rapid deployment of prediction market verticals without requiring fundamental platform restructuring or new regulatory classifications in many jurisdictions. SOFTSWISS has expanded its platform capabilities to address growing operator demand for alternative engagement models.

Strategic Implications for iGaming Stakeholders

Prediction markets represent more than a novel betting vertical – they offer "always-on" wagering opportunities unconstrained by sports seasons or event schedules. Political elections, economic indicators, entertainment awards, and cultural phenomena provide continuous engagement possibilities that complement traditional sports offerings.

The customer acquisition potential is substantial. Prediction market participants often exhibit higher engagement levels and longer session durations compared to traditional sports bettors. The broader range of events attracts demographics that might not engage with sports betting, expanding addressable market sizes for operators.

Risk management considerations differ significantly between prediction market models. Peer-to-peer exchanges require sophisticated liquidity management and market-making capabilities. Fixed-odds implementations allow operators to apply existing risk management frameworks while gradually building expertise in non-sports event assessment.

The regulatory landscape will continue evolving rapidly. Early movers who establish compliant operations in favourable jurisdictions may gain significant competitive advantages as frameworks solidify. However, operators must carefully monitor regulatory developments and maintain flexibility to adapt to changing classifications.

Customer Acquisition Insight

Political prediction markets attract highly educated, affluent demographics who often exhibit 3-5x higher lifetime values compared to traditional sports bettors. These users frequently engage with multiple event types, creating natural cross-selling opportunities across platform verticals.

Market Outlook and Operator Considerations

The prediction markets sector's rapid growth from niche trading to $44 billion in annual volume demonstrates its mainstream viability. Regulatory attention is intensifying globally, but this scrutiny should lead to clearer frameworks rather than blanket restrictions. The sector's financial market roots in many jurisdictions provide legitimacy that pure gambling classifications might not enjoy.

For iGaming operators, the question is not whether prediction markets belong in their product portfolios, but how to implement them effectively while managing regulatory and operational risks. Fixed-odds implementations offer lower-risk entry points, while full exchange capabilities require more substantial commitments but offer greater differentiation potential.

The overlap with existing customer bases, familiar mechanics, and expanding event universes make prediction markets a natural evolution for operators seeking diversification beyond traditional sports betting and casino gaming. As regulatory frameworks mature and implementation barriers decrease, prediction markets may become as fundamental to iGaming platforms as sports betting and online casinos are today.

| Region | Classification | Status | Notes |

|---|---|---|---|

| United States | Financial (derivatives) | Partially regulated | Ongoing debate about potential reclassification under gambling laws |

| Canada | Mixed | Grey area | Operates across Canada except in Ontario, banned in 2025. May be classified as securities, derivatives or both |

| European Union | Varies (often gambling) | Mostly restricted | No unified framework. Many countries (Belgium, France, Italy, Poland, Romania) ban platforms as unlicensed |

| United Kingdom | Gambling | Regulated | Classified as betting platforms requiring Gambling Commission licence |

| Asia | Gambling | Mostly restricted | Restricted in most countries, Singapore blocked access, Thailand moving toward restrictions |

| Oceania | Gambling | Restricted | Banned in Australia as unlicensed activity, prohibited in New Zealand under existing gambling laws |

| South America | Gambling/unclear | Mostly restricted/grey | Argentina and Brazil banned platforms as unlicensed; Chile and Peru are grey areas |

| Africa | Unclear | Grey area | Limited regulatory clarity, but regulatory focus increasing as of early 2025 |

This depends entirely on regulatory classification. In some jurisdictions, prediction markets qualify as financial instruments rather than gambling products, potentially allowing operation under different regulatory frameworks. However, many countries specifically classify them as gambling regardless of structure.

Industry data suggests markets need at least $10,000-50,000 in initial liquidity to maintain reasonable bid-ask spreads. Without sufficient depth, price volatility increases dramatically and discourages participation. Most successful platforms seed new markets with house liquidity before opening to public trading.

Platforms establish detailed resolution criteria before market launch, specifying exact data sources and measurement methodologies. For subjective events, they often use consensus from multiple authoritative sources or expert panels. Clear resolution criteria are essential to prevent disputes and maintain trader confidence.

This varies significantly by jurisdiction and license terms. Some gambling licenses cover event-based wagering broadly enough to include prediction markets, while others specifically exclude non-sporting events. Operators should consult regulatory counsel before expanding into prediction markets under existing licenses.

According to SOFTSWISS.